How to Build Multiple Income Streams (Without Burning Out)

One income source is a vulnerability. Here's how to build multiple revenue streams, from side hustles to passive income, while keeping your sanity intact.

In This Article

Why Relying on One Income Is the Riskiest Thing You Can Do

Most people think of diversification in terms of investments. But the most dangerous lack of diversification isn't in your portfolio. It's in your income.

If 100% of your income comes from one employer, you're one layoff, one restructuring, or one bad quarter away from zero. That's not pessimism. It's basic risk assessment. The average American will go through 3-5 involuntary job transitions in their career.

The wealthiest people rarely rely on a single source. They have salary plus investments plus a side business plus rental income. You don't need all four, but having at least two gives you optionality that changes how you make decisions.

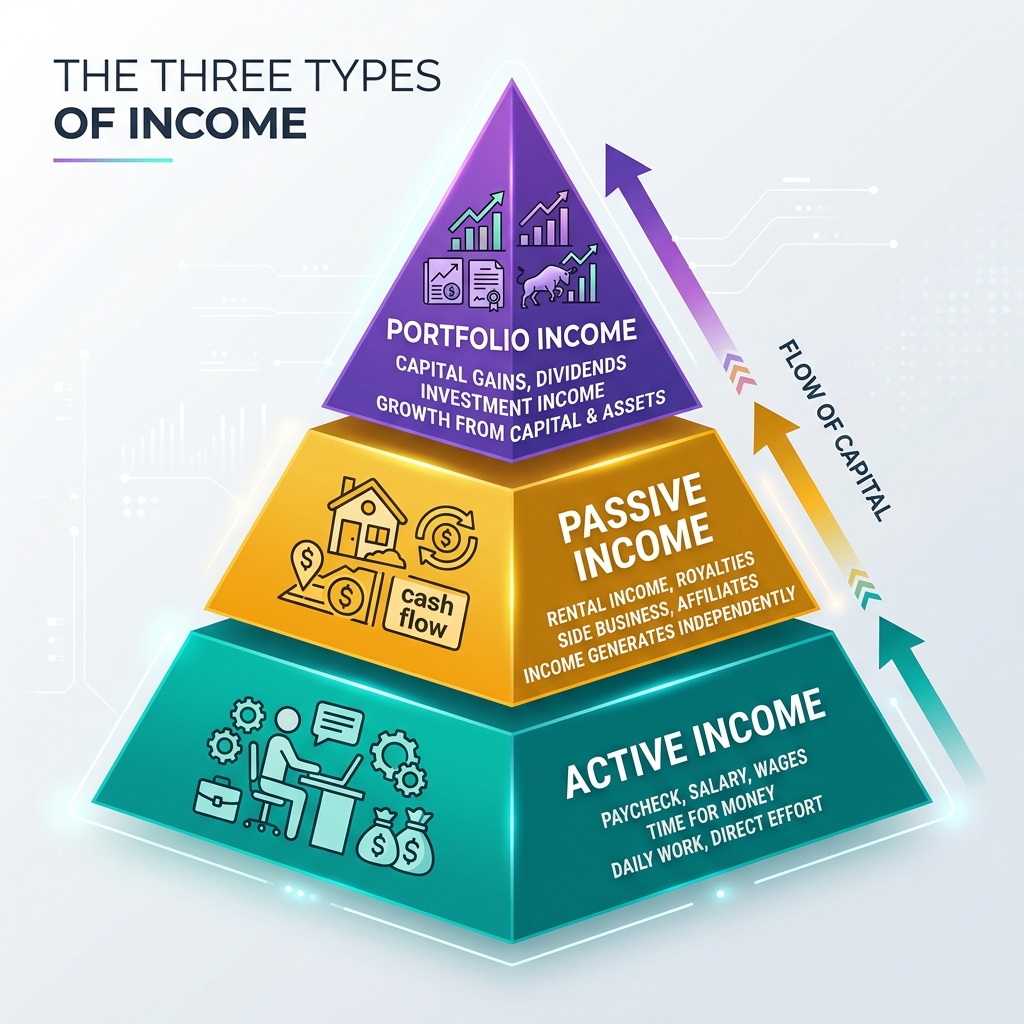

The Three Types of Income (And Which to Prioritize)

Not all income is created equal. Understanding the three types helps you build strategically instead of just working more hours.

Active income is trading time for money: your job, freelancing, consulting. It's the fastest to start but doesn't scale. Passive income requires upfront work or capital but generates returns with minimal ongoing effort, like dividends, rental income, and digital products. Portfolio income comes from investments, including capital gains, interest, and dividends.

The smart sequence: maximize your active income first (it funds everything else), use the surplus to build passive income streams, and let portfolio income compound in the background. Don't try to skip steps.

Realistic Side Hustles That Actually Pay

Let's skip the 'start a dropshipping empire' nonsense. Here are income streams that real people with full-time jobs actually maintain without losing their minds.

Skill-based freelancing is the fastest path to extra income. If you can write, design, code, or do data analysis, platforms like Upwork and Fiverr can generate $500-2,000/month within a few months. The key is niching down. 'I write email sequences for SaaS companies' beats 'I'm a freelance writer' every time.

Digital products have the best long-term ROI. An online course, a Notion template pack, or an ebook takes weeks to create but can sell for years. The marginal cost of each sale is essentially zero.

- Freelance writing, design, or development ($50-150/hour)

- Online tutoring or coaching ($40-100/hour)

- Digital products: courses, templates, ebooks ($500-5,000/month passively)

- Content creation: YouTube, newsletter, blog (slow build, high ceiling)

- Rental income: spare room, parking space, storage ($200-1,500/month)

- Dividend investing: build a portfolio that pays quarterly ($100-1,000/month over time)

The Burnout Trap: How to Add Income Without Losing Your Life

Here's what nobody tells you about multiple income streams: the first year sucks. You're working your day job, coming home tired, and trying to build something on the side. If you're not careful, you'll burn out and quit everything.

The solution is the 'One Thing' rule. Pick ONE additional income stream. Give it 5-10 hours per week. Run it for 6 months before evaluating. If it's working, systematize it. If it's not, pivot. But never run three side hustles simultaneously. That's a recipe for doing everything badly.

Also, automate and delegate early. Use tools, hire a VA for $5/hour, batch your content creation. The goal is to build systems, not just add more work to your plate.

Pro Tip

Track all your income streams in WiseCash. Seeing exactly how much each source contributes helps you double down on winners and cut losers, just like a smart investor does with their portfolio.

The Long Game: From Side Hustle to Financial Freedom

The endgame isn't working four jobs forever. It's building income streams that eventually don't require your active time. A freelance business becomes an agency with contractors. A blog becomes a media business with sponsors. Savings become dividend-producing investments.

Financial independence isn't about retiring early (unless you want to). It's about reaching the point where your passive income covers your expenses, and your job becomes a choice rather than a necessity. That shift in psychology is worth more than any dollar amount.

Start with one stream this month. Not next month, not next year. Pick the option that best fits your skills, commit 6 hours this week, and begin. Every wealthy person you admire started with a single step.

Frequently Asked Questions

What are the best passive income streams for beginners?

The most accessible passive income streams for beginners are: high-yield savings accounts (4-5% APY), dividend index funds (start with SCHD or VYM), and digital products like online courses or templates. These require relatively low upfront capital or one-time effort and generate ongoing returns.

How many income streams should I have?

Start with two: your primary job plus one side income source. Once that's stable, gradually add more. Most financially independent people have 3-5 income streams, but trying to build them all simultaneously leads to burnout. Focus on one at a time.

Take Action

Reading is great.

Tracking is better.

Apply what you've learned with WiseCash — the financial dashboard built for people serious about their money.

Start Tracking Free →Keep Reading

Related Articles

7 Financial Habits of Wealthy People (That Have Nothing to Do With Luck)

Wealth isn't built by lottery winners. It's built by people with boring, consistent habits. Here are the 7 daily practices that separate the wealthy from everyone else.

25 Wealth-Building Rules That Most People Learn Too Late

Discover 25 proven wealth-building rules inspired by Scott Galloway's *The Algebra of Wealth* — from compound investing and smart delegation to the psychology of money and long-term financial freedom.

The 50/30/20 Rule: The Simplest Budget Framework That Actually Works

Stop overcomplicating your budget. The 50/30/20 rule gives you a dead-simple framework to split your income into needs, wants, and savings so you can actually stick with it.