The 50/30/20 Rule: The Simplest Budget Framework That Actually Works

Stop overcomplicating your budget. The 50/30/20 rule gives you a dead-simple framework to split your income into needs, wants, and savings so you can actually stick with it.

In This Article

Why Most Budgets Fail (And Why This One Doesn't)

Let's be honest, most people who try budgeting give up within the first month. They download a spreadsheet, track every single coffee, and burn out by week three. Sound familiar?

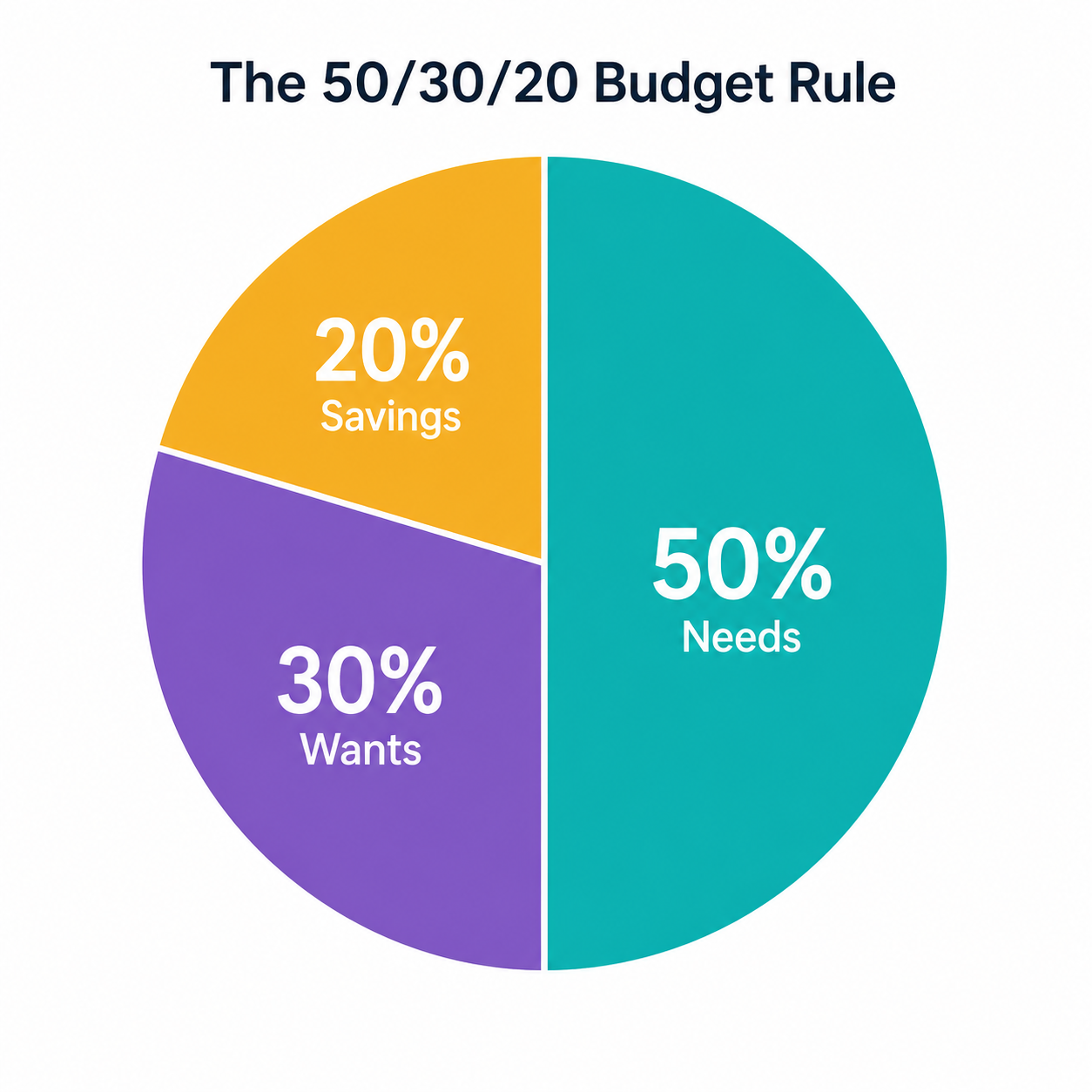

The 50/30/20 rule works because it doesn't ask you to micromanage every dollar. Instead, it gives you three big buckets. That's it. You split your after-tax income into 50% for needs, 30% for wants, and 20% for savings. No color-coded spreadsheets required.

Senator Elizabeth Warren popularized this framework in her book 'All Your Worth,' and it's stuck around because it's flexible enough for real life but structured enough to actually move the needle on your finances.

The 50/30/20 split visualized. Simple, clear, effective.

The 50% Bucket: Needs (Non-Negotiables)

Half of your take-home pay goes to the stuff you literally can't skip. Rent or mortgage. Utilities. Groceries (not dining out, that falls under wants). Insurance. Minimum debt payments. Transportation to work.

Here's the litmus test: if you'd be in serious trouble without it within a month, it's a need. Everything else is negotiable.

If your needs eat up more than 50%, that's a red flag, not a moral failing. It usually means your housing costs are too high relative to income, which is extremely common in major cities. The fix isn't shame; it's strategy.

Pro Tip: Use WiseCash's automatic transaction categorization to instantly see what percentage of your income goes to needs vs. wants. No manual sorting required.

Rent or mortgage payments

Utilities (electricity, water, internet)

Groceries and essential household items

Health insurance and medical necessities

Minimum loan and credit card payments

Transportation (car payment, gas, public transit)

The 30% Bucket: Wants (The Fun Stuff)

This is the part most budgeting advice gets wrong. They tell you to cut all discretionary spending. That's a recipe for misery, and eventually, a revenge shopping spree.

The 30% wants bucket is permission to enjoy your money. Dining out, streaming subscriptions, hobbies, travel, that overpriced oat milk latte. All fair game. The key is keeping it within the boundary.

A want is anything that improves your quality of life but isn't strictly necessary for survival. The line between needs and wants can get blurry (is a gym membership a need?), and that's okay. Be honest with yourself, not perfect.

The 20% Bucket: Savings & Debt Payoff

This is where wealth actually gets built. Twenty percent of your income goes toward your future self: emergency fund, retirement accounts, extra debt payments above the minimum, or investing.

The order matters. If you don't have an emergency fund covering 3-6 months of expenses, that comes first. Then attack high-interest debt. Then invest. Trying to do all three at once with 20% usually means none of them get done well.

And if 20% feels impossible right now? Start with 5%. Then bump it by 1% every month. The habit matters more than the number.

Even modest savings rates compound dramatically over time.

Pro Tip: Set up automatic transfers on payday. Money you never see is money you never spend. WiseCash can track your savings velocity and tell you exactly when you'll hit your goals.

How to Adapt the 50/30/20 Rule to Your Reality

The beauty of this framework is its flexibility. Living in an expensive city where rent alone eats 40% of your income? Maybe your split looks more like 60/20/20. Earning well and living modestly? Try 40/20/40 and fast-track your financial independence.

The ratios are guidelines, not commandments. What matters is that you have a system, you know where your money goes, and you're consistently putting something toward your future.

Review your split every quarter. Life changes. You get a raise, move cities, or have a kid. Your budget should evolve too.

High cost of living? Try 60/20/20 and focus on increasing income

Aggressive saver? Flip it to 40/20/40 for faster wealth building

Paying off debt? Consider 50/20/30 with the extra 10% on debt

Variable income? Base your percentages on your lowest earning month

Frequently Asked Questions

What is the 50/30/20 budget rule?

The 50/30/20 rule is a budgeting framework where you allocate 50% of your after-tax income to needs (housing, groceries, utilities), 30% to wants (dining out, entertainment, hobbies), and 20% to savings and debt repayment. It was popularized by Senator Elizabeth Warren.

Is the 50/30/20 rule good for beginners?

Yes, the 50/30/20 rule is one of the best budgeting methods for beginners because it's simple, flexible, and doesn't require tracking every individual purchase. You only need to categorize spending into three broad buckets.

What if I can't save 20% of my income?

Start where you can. Even 5% is better than nothing. Increase your savings rate by 1% each month as you find ways to reduce expenses or increase income. The habit of saving consistently matters more than the exact percentage.

Take Action

Reading is great.

Tracking is better.

Apply what you've learned with WiseCash — the financial dashboard built for people serious about their money.

Start Tracking Free →Keep Reading

Related Articles

How to Build an Emergency Fund Fast (Even on a Tight Budget)

An emergency fund isn't optional. It's the foundation of every solid financial plan. Here's a practical, no-fluff guide to building yours from scratch.

How to Build Multiple Income Streams (Without Burning Out)

One income source is a vulnerability. Here's how to build multiple revenue streams, from side hustles to passive income, while keeping your sanity intact.

Snowball vs. Avalanche: The Two Best Strategies to Crush Your Debt

Drowning in debt? Two proven methods can get you out. Here's an honest comparison of the Snowball and Avalanche strategies, and which one will actually work for you.