How to Build an Emergency Fund Fast (Even on a Tight Budget)

An emergency fund isn't optional. It's the foundation of every solid financial plan. Here's a practical, no-fluff guide to building yours from scratch.

In This Article

Why Your Emergency Fund Is Your Most Important Financial Asset

Forget investments. Forget side hustles. Before any of that matters, you need cash you can access when life hits you with something unexpected. And it will.

A car breakdown. An unexpected medical bill. A layoff that comes out of nowhere. Without an emergency fund, these aren't just inconveniences. They're financial catastrophes that force you into credit card debt or worse.

According to a 2025 Bankrate survey, 44% of Americans can't cover an unexpected $1,000 expense without borrowing. That's not a personal failure. It's a systemic gap in financial education. Let's fix it.

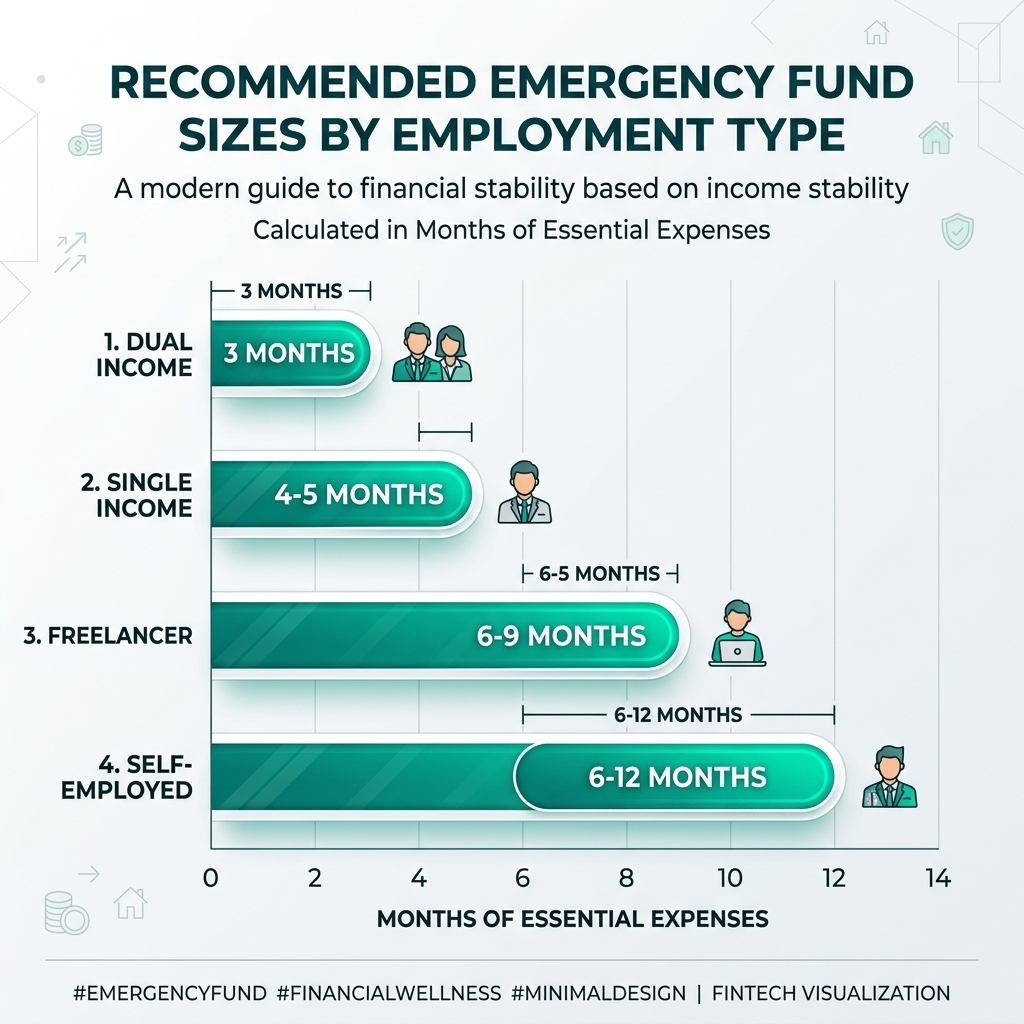

How Much Do You Actually Need?

The classic advice is 3 to 6 months of essential living expenses. Not income, but expenses. There's a big difference. If you earn $5,000/month but your essential bills are $3,200, your target is $9,600 to $19,200.

But here's the thing: even $1,000 is transformative. It's the difference between putting a car repair on a credit card at 24% APR and just handling it. Don't let the perfect number stop you from starting.

Your magic number depends on your situation. Freelancers and gig workers should aim for 6+ months. Dual-income households with stable jobs might be comfortable at 3 months. Single-income families should target the higher end.

- Stable dual income: 3 months of expenses

- Stable single income: 4-5 months of expenses

- Freelancer or gig worker: 6-9 months of expenses

- Self-employed business owner: 6-12 months of expenses

The $1,000 Sprint: Your First Milestone

Don't aim for 6 months right away. That number feels impossible when you're starting from zero and it kills motivation. Instead, sprint to $1,000. That's your first real financial safety net.

Here's how to get there fast: audit your subscriptions (you're probably paying for at least two things you forgot about), sell stuff you don't use, temporarily cut one discretionary expense, and throw every unexpected dollar at it. Tax refunds, birthday money, cash back rewards. All of it.

Most people can hit $1,000 in 30-60 days with focus. Once you get there, the psychological shift is huge. You go from 'I have nothing' to 'I can handle a surprise.' That confidence compounds.

Pro Tip

Use WiseCash to set a $1,000 savings goal and track your progress in real-time. Seeing that progress bar fill up is genuinely motivating.

Where to Keep Your Emergency Fund

Your emergency fund has one job: be there when you need it. That means it should be liquid (easily accessible), safe (no market risk), and separate from your checking account so you don't accidentally spend it.

A high-yield savings account (HYSA) is the gold standard. As of early 2026, many are offering 4.5-5% APY, which means your safety net is actually growing while it waits. Look at Marcus by Goldman Sachs, Ally Bank, or Capital One 360.

Don't invest your emergency fund. Not in stocks, not in crypto, not in your cousin's startup. This isn't money meant to grow. It's money meant to be there. Period.

- High-yield savings account (HYSA): best balance of access and growth

- Money market account: slightly higher rates, same liquidity

- Regular savings account: fine if HYSA isn't available to you

- DO NOT put it in: stocks, crypto, CDs with penalties, or under your mattress

Automate It and Forget It

The single best thing you can do for your emergency fund is make it automatic. Set up a recurring transfer from your checking to your HYSA on payday. Even $25 per paycheck adds up to $650/year.

Treat this transfer like a bill. Non-negotiable. You adapt to the slightly smaller checking balance within two weeks, guaranteed. It's the financial equivalent of 'out of sight, out of mind.'

Once you hit your target, don't stop completely. Reduce the auto-transfer and redirect the rest toward investments or debt payoff. But keep that fund topped up, because you will need it eventually.

Pro Tip

The 'pay yourself first' method works because it removes willpower from the equation. You can't spend money that's already been moved.

Frequently Asked Questions

How much should I have in my emergency fund?

Most financial experts recommend 3 to 6 months of essential living expenses. However, even $1,000 provides meaningful protection against unexpected costs like car repairs or medical bills. Your ideal amount depends on job stability, income sources, and family situation.

Where should I keep my emergency fund?

A high-yield savings account (HYSA) is the best option for most people. It offers easy access, FDIC insurance, and competitive interest rates (4-5% APY in 2026). Avoid investing your emergency fund in stocks or crypto. This money needs to be safe and accessible.

Should I pay off debt or build an emergency fund first?

Build a small emergency fund of $1,000 first, then aggressively pay off high-interest debt, then finish building your full emergency fund. Without any savings buffer, unexpected expenses will just create more debt.

Take Action

Reading is great.

Tracking is better.

Apply what you've learned with WiseCash — the financial dashboard built for people serious about their money.

Start Tracking Free →Keep Reading

Related Articles

The 50/30/20 Rule: The Simplest Budget Framework That Actually Works

Stop overcomplicating your budget. The 50/30/20 rule gives you a dead-simple framework to split your income into needs, wants, and savings so you can actually stick with it.

How to Build Multiple Income Streams (Without Burning Out)

One income source is a vulnerability. Here's how to build multiple revenue streams, from side hustles to passive income, while keeping your sanity intact.

Snowball vs. Avalanche: The Two Best Strategies to Crush Your Debt

Drowning in debt? Two proven methods can get you out. Here's an honest comparison of the Snowball and Avalanche strategies, and which one will actually work for you.