Snowball vs. Avalanche: The Two Best Strategies to Crush Your Debt

Drowning in debt? Two proven methods can get you out. Here's an honest comparison of the Snowball and Avalanche strategies, and which one will actually work for you.

In This Article

The Debt Crisis No One Talks About at Dinner

Total U.S. consumer debt hit $17.9 trillion in 2025. Average credit card balance: $6,500 at 24% APR. If those numbers make you feel less alone, good. Because debt is insanely common and deeply misunderstood.

The shame around debt keeps people stuck. They ignore statements, make minimum payments, and hope the problem somehow resolves itself. It won't. But with the right strategy, you can systematically eliminate every dollar and actually feel good doing it.

Two methods dominate the debt payoff world: the Debt Snowball and the Debt Avalanche. Both work. They just work differently. Let's break down which one fits your brain.

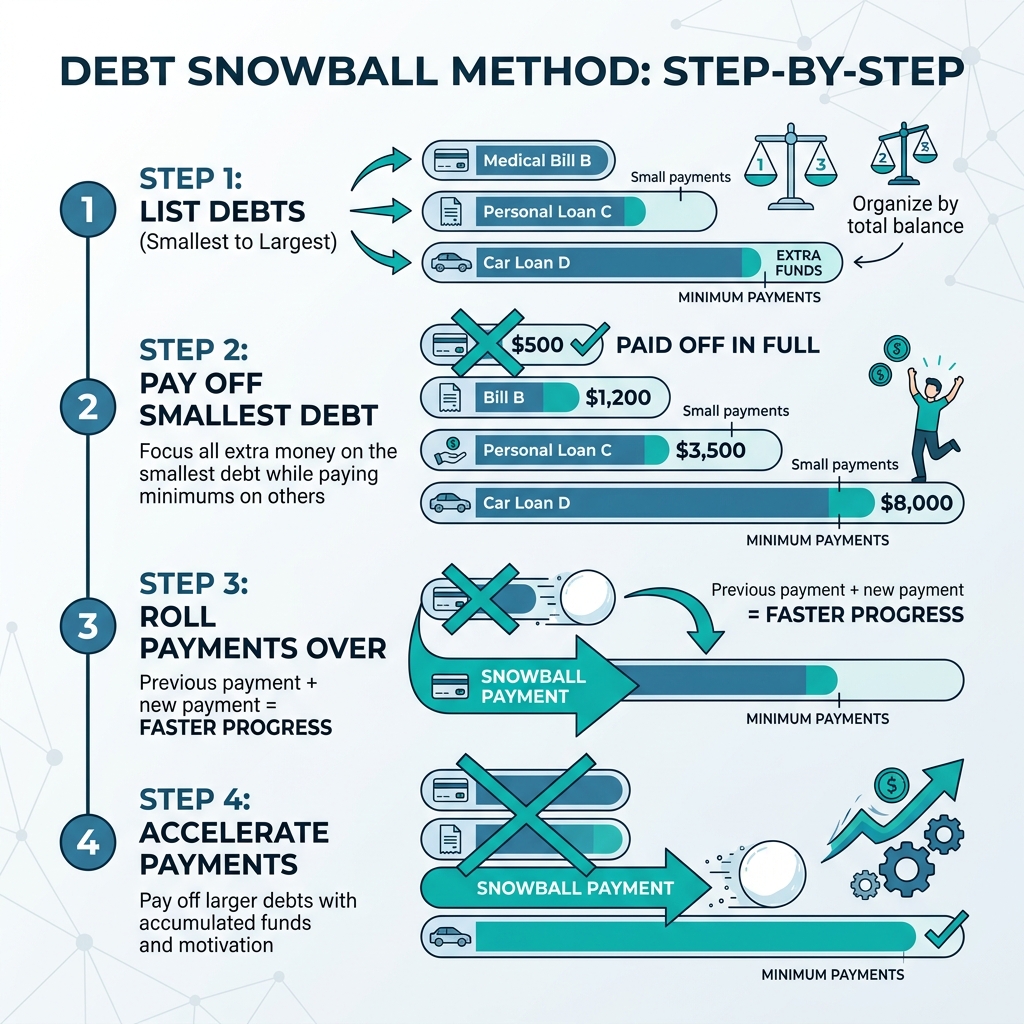

The Debt Snowball: Momentum Through Quick Wins

Popularized by Dave Ramsey, the Snowball method ignores interest rates entirely. Instead, you list your debts from smallest balance to largest, make minimum payments on everything, and throw every extra dollar at the smallest debt first.

Once that smallest debt is gone (and it will be, fast), you take the payment you were making on it and add it to the next smallest. Your payment 'snowballs' as each debt disappears.

The Snowball isn't mathematically optimal, and you'll pay more in total interest. But it's psychologically brilliant. Those early wins create dopamine hits that keep you motivated. And in personal finance, motivation matters more than math. A perfect plan you abandon is worse than a good plan you stick with.

Pro Tip

The Snowball works best for people who've tried and failed other methods. If you need motivational fuel, start here.

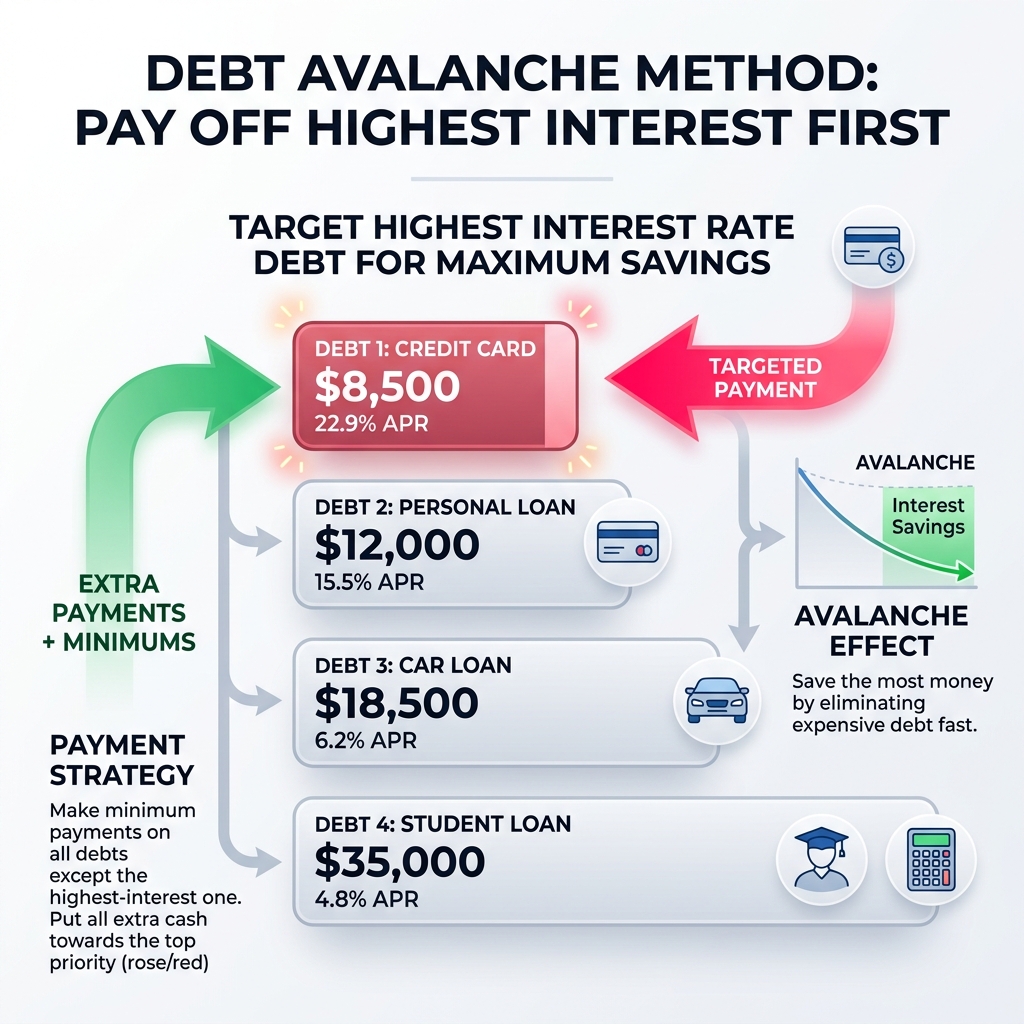

The Debt Avalanche: Mathematically Optimal Payoff

The Avalanche method is the accountant's favorite. You list debts by interest rate from highest to lowest, make minimums on everything, and attack the highest-rate debt first.

By targeting the most expensive debt, you minimize total interest paid. On a $30,000 debt load, the Avalanche can save $1,000-3,000 in interest compared to the Snowball. The bigger your debts and the wider the rate spread, the more you save.

The downside? Your highest-rate debt might also be your largest, which means it could take months before you eliminate your first account. For some people, that long wait kills motivation. Know yourself before choosing.

Head-to-Head: Which Strategy Wins?

Let's compare with a real example. Say you have three debts: a $500 medical bill at 0% APR, a $3,000 credit card at 24% APR, and a $10,000 personal loan at 8% APR. You have $500/month total to allocate toward debt.

Snowball order: medical bill, then credit card, then personal loan. You'd be debt-free in 28 months, paying about $2,800 in total interest.

Avalanche order: credit card, then personal loan, then medical bill. Debt-free in 27 months, paying about $2,200 in interest. The Avalanche saves $600 and one month. Meaningful, but not life-changing.

The real answer? The best method is the one you'll actually follow through on. If you've never successfully paid off a debt before, go Snowball. If you're disciplined and motivated by optimization, go Avalanche.

- Snowball: Best for motivation, people who've struggled with debt before

- Avalanche: Best for math-oriented people, large debts with high rate spreads

- Hybrid: Pay off one tiny debt for a quick win, then switch to Avalanche

- Both require: stopping new debt accumulation (cut the credit cards if needed)

The Rules That Apply No Matter Which Method You Choose

First rule: stop accumulating new debt. If you're paying off your credit card while still swiping it for dinners out, you're filling a bathtub with the drain open. Consider a temporary spending freeze on non-essentials.

Second: build a tiny emergency fund ($1,000) before aggressively paying debt. Otherwise, one car repair sends you right back into the hole.

Third: automate your extra payments. Manual payments get 'forgotten' when something more fun comes along. Set it and protect it.

Fourth: celebrate milestones. Paid off your first card? Do something small that makes you happy. This isn't about deprivation. It's about strategic allocation. The discipline is in the system, not in suffering.

Pro Tip

Use WiseCash to track every debt payment and watch your balances drop in real time. Nothing feels better than seeing that line chart trend toward zero.

Frequently Asked Questions

Which is better: the debt snowball or debt avalanche method?

The debt avalanche saves more money on interest by targeting high-rate debts first, while the debt snowball builds motivation through quick wins by paying off smallest balances first. Research shows both methods work, and the best choice depends on your personality. If you need motivation, choose Snowball. If you're disciplined and want to minimize cost, choose Avalanche.

How long does it take to pay off $10,000 in credit card debt?

With minimum payments only at 24% APR, it could take 20+ years. Using the Avalanche method and paying $500/month, you could be debt-free in about 24 months. Using the Snowball method might take 1-2 months longer but provides motivational wins along the way.

Should I save or pay off debt first?

Build a small $1,000 emergency fund first to prevent new debt from unexpected expenses. Then aggressively pay off high-interest debt (above 7-8%). Once high-interest debt is gone, split extra money between building a full emergency fund and investing.

Take Action

Reading is great.

Tracking is better.

Apply what you've learned with WiseCash — the financial dashboard built for people serious about their money.

Start Tracking Free →Keep Reading

Related Articles

How to Build Multiple Income Streams (Without Burning Out)

One income source is a vulnerability. Here's how to build multiple revenue streams, from side hustles to passive income, while keeping your sanity intact.

The 50/30/20 Rule: The Simplest Budget Framework That Actually Works

Stop overcomplicating your budget. The 50/30/20 rule gives you a dead-simple framework to split your income into needs, wants, and savings so you can actually stick with it.

A No-BS Beginner's Guide to Investing (Start With $100)

Investing isn't just for Wall Street bros. Here's how to start building real wealth with index funds and ETFs, even if you only have $100 to spare.